My poking and probing shows that when the assumptions are changed to less optimistic but still reasonable scenarios, the models can swing to much lower profit levels or even losses.

My latest Poynter e-Media Tidbits column

Showing posts with label Finance. Show all posts

Showing posts with label Finance. Show all posts

Help Price 'Finance for Media Professionals'

It's surprising to me how difficult it can be not to produce a great seminar but rather to figure out how to price it. Pricing, of course, is a science in itself with people getting Phd's to figure out its ins and outs and teach it at prestigious business schools. My partner at Scribe Media, Peter Cervieri (a graduate of one of those schools), has written a very open post on the Scribe site talking about some discussions he and I have been having about how to price our 'Finance for Media Professionals' video course.

I'd be grateful for your feedback. The post is here. You can comment there or below.

We have to cover our costs, and also want to make the video as widely available as possible. We want to make at least some profit. Price it low, and we might sell more copies. Price it higher, and we may sell fewer but make more money. Those who attended the shoot told us they thought we could charge $149-$179.

I'd be grateful for your feedback. The post is here. You can comment there or below.

We have to cover our costs, and also want to make the video as widely available as possible. We want to make at least some profit. Price it low, and we might sell more copies. Price it higher, and we may sell fewer but make more money. Those who attended the shoot told us they thought we could charge $149-$179.

Changes More Fundamental Than News

In Clay Shirky’s essay on what will sustain the news business, he writes this:

Shirky goes on to frame today’s “experiments” -- Wikipedia, Craigslist -- as equivalent to experiments in the age of the Gutenberg bible that led to the reordering of civilization. (Widespread literacy ultimately led to the protestant reformation and doubts cast upon writings of the ancients, Shirky writes, quoting other scholars.)

Today’s experiments are many. We don’t often talk about the ones that have failed, though there are many more of those than the Googles, MySpaces, Craigslists or Wikipedias (assuming you’re willing to confirm them as successes, nascent though they may be). Even experiments that may prove to be economic failures -- there’s no guarantee that either Facebook or Twitter will become self-sustaining -- have been so disruptive as to rend the fabric of the previous media orders. They are bringing about new forms of communication, technology and interaction that are fundamentally changing human behavior. Those able to harness these forces are finding themselves armed with great power to sway people, and earn a few bucks. Just ask President Obama. LINK

We don’t know what experiments will bear fruit today. The foundation model, citizen-funded journalism, micro-payments to solo operators, advertisers, subscriptions for high-end information. We do know, as Bill Battino acknowledged as I held up the report his research team at IBM had produced that will be available Monday for free, that information may not want to be free but it is (genuflection toward Chris Anderson) moving in that direction.

I put this disruption of news against the backdrop of the severe disruption of a financial system whose reward system has for decades been based on scarcity, control of and limits to information (why do you think traders will pay $1,200 - $1,600 for a Thomson Reuters or Bloomberg terminal on their desks?). We see in the anger over the relatively paltry revelation of the AIG bonuses how clouded and guarded information is, how hard it is even for analysts poring over disclosure statements filed with the SEC to figure out exactly what’s going on. (A significant amount of my MBA coursework was spent on ferreting out the hidden morsels in annual and quarterly reports that corporate officers are legally bound to report but are trying through obfuscation to hide.)

Not only do I think the information disruption will be much farther and wider than to the news business, but I also think this pressure is going to lead to changes in the way we handle finance, perhaps business in general. Imagine if there were transparency in the investment banking, private equity and venture capital worlds. How much less of a margin would the people in those worlds make? How would it change behaviors if the arbitrage was open and visible to all?

I don’t know. Nobody knows. We’re collectively living through 1500, when it’s easier to see what’s broken than what will replace it. The internet turns 40 this fall. Access by the general public is less than half that age. Web use, as a normal part of life for a majority of the developed world, is less than half that age. We just got here. Even the revolutionaries can’t predict what will happen.

Shirky goes on to frame today’s “experiments” -- Wikipedia, Craigslist -- as equivalent to experiments in the age of the Gutenberg bible that led to the reordering of civilization. (Widespread literacy ultimately led to the protestant reformation and doubts cast upon writings of the ancients, Shirky writes, quoting other scholars.)

Today’s experiments are many. We don’t often talk about the ones that have failed, though there are many more of those than the Googles, MySpaces, Craigslists or Wikipedias (assuming you’re willing to confirm them as successes, nascent though they may be). Even experiments that may prove to be economic failures -- there’s no guarantee that either Facebook or Twitter will become self-sustaining -- have been so disruptive as to rend the fabric of the previous media orders. They are bringing about new forms of communication, technology and interaction that are fundamentally changing human behavior. Those able to harness these forces are finding themselves armed with great power to sway people, and earn a few bucks. Just ask President Obama. LINK

We don’t know what experiments will bear fruit today. The foundation model, citizen-funded journalism, micro-payments to solo operators, advertisers, subscriptions for high-end information. We do know, as Bill Battino acknowledged as I held up the report his research team at IBM had produced that will be available Monday for free, that information may not want to be free but it is (genuflection toward Chris Anderson) moving in that direction.

I put this disruption of news against the backdrop of the severe disruption of a financial system whose reward system has for decades been based on scarcity, control of and limits to information (why do you think traders will pay $1,200 - $1,600 for a Thomson Reuters or Bloomberg terminal on their desks?). We see in the anger over the relatively paltry revelation of the AIG bonuses how clouded and guarded information is, how hard it is even for analysts poring over disclosure statements filed with the SEC to figure out exactly what’s going on. (A significant amount of my MBA coursework was spent on ferreting out the hidden morsels in annual and quarterly reports that corporate officers are legally bound to report but are trying through obfuscation to hide.)

Not only do I think the information disruption will be much farther and wider than to the news business, but I also think this pressure is going to lead to changes in the way we handle finance, perhaps business in general. Imagine if there were transparency in the investment banking, private equity and venture capital worlds. How much less of a margin would the people in those worlds make? How would it change behaviors if the arbitrage was open and visible to all?

Cash is OK

I've worked with a number of companies whose owners agonized over having too much cash on the books -- and who were sometimes urged to take on more debt, get rid of the cash, reinvest, grow-grow-grow (beyond even a very high IRR -- a way of calculating returns with cash on hand).

Well, Activision apparently has $3 billion in cash and is ready to spend to shore up its video game line. Cash doesn't look so silly any more, does it?

Well, Activision apparently has $3 billion in cash and is ready to spend to shore up its video game line. Cash doesn't look so silly any more, does it?

Seminar: Finance for Media Professionals

Dorian's Teeming Media is sponsoring the following course. It's a great deal.

The budget in an organization doesn’t go to the best projects. It goes to good projects that are best presented in financial terms. The more you understand about how the company makes financial decisions, the greater your ability is to get the funding.

In these financially distressed times, you need more than ever to:

* understand the way money flows in your organization;

* bolster your financial skills and learn the finance behind decision-making;

* know how to interpret budgets, secure funds, earn revenue, and do more with available resources.

Whether you’re a creative media professional, an advertising executive, a producer, a publisher, an entrepreneur or in any other area of the media industry, this seminar will help you build skills that will make you more valuable, help you keep the job you have, get a new job, secure new business and make you a stronger competitor in today’s marketplace.

In less than three hours, we will teach you in depth how to read and understand:

* Balance Sheets;

* Income Statements;

* Cash Flow Statements;

and, crucially, why you should care about all of them.

Register here! Only 15 Seats Available. Special $50 rate for an intensive 3-hour seminar. March 23, 6-9 p.m.

The budget in an organization doesn’t go to the best projects. It goes to good projects that are best presented in financial terms. The more you understand about how the company makes financial decisions, the greater your ability is to get the funding.

In these financially distressed times, you need more than ever to:

* understand the way money flows in your organization;

* bolster your financial skills and learn the finance behind decision-making;

* know how to interpret budgets, secure funds, earn revenue, and do more with available resources.

Whether you’re a creative media professional, an advertising executive, a producer, a publisher, an entrepreneur or in any other area of the media industry, this seminar will help you build skills that will make you more valuable, help you keep the job you have, get a new job, secure new business and make you a stronger competitor in today’s marketplace.

In less than three hours, we will teach you in depth how to read and understand:

* Balance Sheets;

* Income Statements;

* Cash Flow Statements;

and, crucially, why you should care about all of them.

Register here! Only 15 Seats Available. Special $50 rate for an intensive 3-hour seminar. March 23, 6-9 p.m.

More on Media Money

A few consistent themes over two days at the AlwaysOn, OnMedia conference yesterday and today from venture capitalists, bankers and other investors:

- If you invest, you’ll have to invest for the longer term -- people aren’t kicking in as easily with subsequent rounds. (Echoes earlier remarks by David Rose and others.)

- There’s so little surety in the market, that people aren’t wiling to say what a deal is worth, how many deals they’ll do, and have very little visibility into the future. “If Microsoft can’t predict next quarter results, how can we?” one banker told me. When I asked a panel to give any specific numbers -- from valuations to expected dollars to number of deals, anything they were wiling to share for what they saw in ‘09-- they instead said that the nature of the deals had changed.

- The previous assumptions and equations for measuring a deal’s worth are way out of whack. Steve Fletcher, Managing Director, GCA Savvian, said that while debt was previously measured at seven percent (the interest rate on a loan), it was now as high as 22 percent, and that equity risk, previously measured at 5-7 percent, was now “a much bigger number.”

- Money people have a more free time now. Jay MacDonald a partner at media bankers DeSilva & Phillips joked when there weren’t questions coming to his panel on media M&A: “Come on, we have time. Bring in some lunch.”

- Deal prices are down, investors are in a better position to demand better terms (Series B rounds at Series A pricing, for example.)

- At the same time, those looking to sell companies aren’t yet willing to sell at the lower valuations. “Six months ago you were ‘worth x’ and today you’re worth .5x. It’s tough to get your arms around .5x. It’s going to take a while for companies to rationalize that, says Tom Patterson, CEO, Wize.

- Early round investors “have to be prepared to invest every year for fives years,” says Bob Greene, Partner, Contour Venture Partners. (The angels, to make their original investment pay off, will keep investing in a business that can grow.) see point one, above.

- Businesses that are doing well in this environment are ones helping generate sales -- sales leads, targeting, and the like, “business models able to deliver highly qualified leads in a marketplace where people want to be very efficient with their spends,” MacDonald said.

What the Economy Means for Media Investment

Investors here at the AlwaysOn media conference have been confirming in private discussions and on stage what angel investor David Rose said recently: that their money is having to stretch farther, that others are reluctant to come into the rounds as early.

One venture capital investor also told me he’s seeing “A Series pricing” for B and C rounds, meaning that people investing even later in a company’s life cycle are able to, for their money, get a larger share of the equity. For example, instead of getting 15 percent of the company, they’re able to get a fifth of it, he said.

But in a sign of optimism, another, based in Silicon Valley, said that funds of money that were raised 1-2 years ago are still uninvested, so they will need soon to find something to invest in in the next few months.

Later, on a panel about later-stage venture capital investment, Alan Spoon, Managing General Partner of Polaris Venture Partners, said he was seeing more funds looking to others for liquidity, trying to shore up balance sheets and less interested in such calculations as ROI (return on investment -- which in the financial world is a more specific ratio than often gets thrown around in advertising) and IRR, another ratio that figures out the internal rate of return -- how much a company is supposed to be able to earn from the money it has.

The pressures on the markets are making hedge funds and mutual funds get out of the venture game, the panelists also said, and money is being lent and companies being valued at much lower valuations than before the bust.

One venture capital investor also told me he’s seeing “A Series pricing” for B and C rounds, meaning that people investing even later in a company’s life cycle are able to, for their money, get a larger share of the equity. For example, instead of getting 15 percent of the company, they’re able to get a fifth of it, he said.

But in a sign of optimism, another, based in Silicon Valley, said that funds of money that were raised 1-2 years ago are still uninvested, so they will need soon to find something to invest in in the next few months.

Later, on a panel about later-stage venture capital investment, Alan Spoon, Managing General Partner of Polaris Venture Partners, said he was seeing more funds looking to others for liquidity, trying to shore up balance sheets and less interested in such calculations as ROI (return on investment -- which in the financial world is a more specific ratio than often gets thrown around in advertising) and IRR, another ratio that figures out the internal rate of return -- how much a company is supposed to be able to earn from the money it has.

The pressures on the markets are making hedge funds and mutual funds get out of the venture game, the panelists also said, and money is being lent and companies being valued at much lower valuations than before the bust.

Spend Less, Gain Market Share

"When you’re comparing yourself to companies that are spending ‘like drunks,’ you should take comfort, because market share will come to you merely by outlasting them."-- Richard de Silva, General Partner, Highland Capital Partners, at the AlwaysOn OnMedia conference in New York

David Rose: Investments Need To Generate Cash

David Rose, NY Angels founder and head of investment incubator RoseTech Ventures, says his potential portfolio companies today must make money in a way they didn’t have to a year ago.

In early 2008, Rose would help start a business presuming venture capitalists and others would soon come kick in more. Today, “we can’t assume there will be anyone after us with a follow-on round,” he said at a NY:MIEG breakfast event at the Samsung Experience in the Time Warner Center at Columbus Circle. “We are really only looking at businesses that can get to profitability” on their own, and show growth, then, perhaps, get more investment in 2-3 years. The panel, titled, “The Economic Downturn’s Impact on Media & Entertainment,” explored how business has changed for media and technology businesses in recent months, and what prospects may be.

Rose was on the panel with Andrew Cleland, Executive Director of Alliances and Technology Strategy of Time Warner, and Robert Rechti, who is a senior VP and Industry Advisor for GE Commercial Finance’s Media, Communications and Entertainment business. Dale Peskin, co-founder of iFOCOS, host of February’s We Media conference in Miami, moderated. Cleland and Rechti both said they hold to the same principles as before the economy tanked, doing due diligence, though they may now look for more cash flow and flexible business plans, and be more selective in their deals.

(Note: My company, Teeming Media, has done business with both NY:MIEG and We Media.)

In early 2008, Rose would help start a business presuming venture capitalists and others would soon come kick in more. Today, “we can’t assume there will be anyone after us with a follow-on round,” he said at a NY:MIEG breakfast event at the Samsung Experience in the Time Warner Center at Columbus Circle. “We are really only looking at businesses that can get to profitability” on their own, and show growth, then, perhaps, get more investment in 2-3 years. The panel, titled, “The Economic Downturn’s Impact on Media & Entertainment,” explored how business has changed for media and technology businesses in recent months, and what prospects may be.

Rose was on the panel with Andrew Cleland, Executive Director of Alliances and Technology Strategy of Time Warner, and Robert Rechti, who is a senior VP and Industry Advisor for GE Commercial Finance’s Media, Communications and Entertainment business. Dale Peskin, co-founder of iFOCOS, host of February’s We Media conference in Miami, moderated. Cleland and Rechti both said they hold to the same principles as before the economy tanked, doing due diligence, though they may now look for more cash flow and flexible business plans, and be more selective in their deals.

(Note: My company, Teeming Media, has done business with both NY:MIEG and We Media.)

Does NY Mag Understand Newsweek's Business?

In New York Magazine's "numerical summary" of our economic times, they list the decline in the number of cars and light trucks sold, the proposed rise in the price of a transit farecard ... And the decline in guaranteed circulation for Newsweek magazine from 3.1 million in 2007 to a proposed 1.6 million in 2009.

But there's something the writers miss. Not only do they for some reason neglect 2008 (reported base of 2.6 million), but they also leave out a reasonable argument for the newsweekly to be cutting its circ: cutting costs, and the ability to raise ad rates for a more choice audience. As Ad Age reports:

So, while one could look at the move by Newsweek as an act of desperation brought on by declining economic times, we should also note that the company's rate base cut -- something Time did a couple years ago -- has been rumored since well before the current economic decline . It can get a smaller more valuable audience in print, leaving the less valuable but higher numerical audience, a lower-priced commodity for advertisers, to its digital side.

It's safe to say, too, that Newsweek isn't the only magazine thinking along these lines.

But there's something the writers miss. Not only do they for some reason neglect 2008 (reported base of 2.6 million), but they also leave out a reasonable argument for the newsweekly to be cutting its circ: cutting costs, and the ability to raise ad rates for a more choice audience. As Ad Age reports:

Newsweek will likely take the opportunity to simultaneously steer toward a more a elite readership -- by eliminating the least-valuable, most-discounted subscriptions on its books.Times are tough for print pubs, and magazines in recent months have started suffering some of the same steep declines newspapers have gotten used to. But it's also no secret that to get subscriptions, general interest weeklies and monthlies have practically given away the "book" for subscription prices that don't pay for the editions and thrown in premiums (such as umbrellas or tote bags) that can cost a good chunk of the subscription price.

So, while one could look at the move by Newsweek as an act of desperation brought on by declining economic times, we should also note that the company's rate base cut -- something Time did a couple years ago -- has been rumored since well before the current economic decline . It can get a smaller more valuable audience in print, leaving the less valuable but higher numerical audience, a lower-priced commodity for advertisers, to its digital side.

It's safe to say, too, that Newsweek isn't the only magazine thinking along these lines.

Why Online Ads Won't Tank as Badly This Time

Henry Blodget at Silicon Alley Insider writes that we'll see a decline in online advertising (especially display) in '09, but it won't be as bad as the decline in the early part of the decade. He gives a few reasons.

Another reason Web advertising won't tank as bad as the last time is because this time marketers understand they need to be online, and their target audiences are there.

Another reason Web advertising won't tank as bad as the last time is because this time marketers understand they need to be online, and their target audiences are there.

David Rose Tells me What He Taught Me

David left the below in the comments, but I'm bringing it out front, because it's a great clarification and enhancement to what I had written:

1) The Most Important Person on the Startup Team

In a blog post that I wrote on the subject after it came up in a conversation on the nextNY mailing list, I posit that it's not "the techie", nor "the UI person" nor even "the biz guy"...but rather The Entrepreneur... someone with a special set of skils and characteristics that may—or may not—be co-resident with the other functional skills mentioned above.

2) The Ten Crucial Attributes of an Entrepreneur

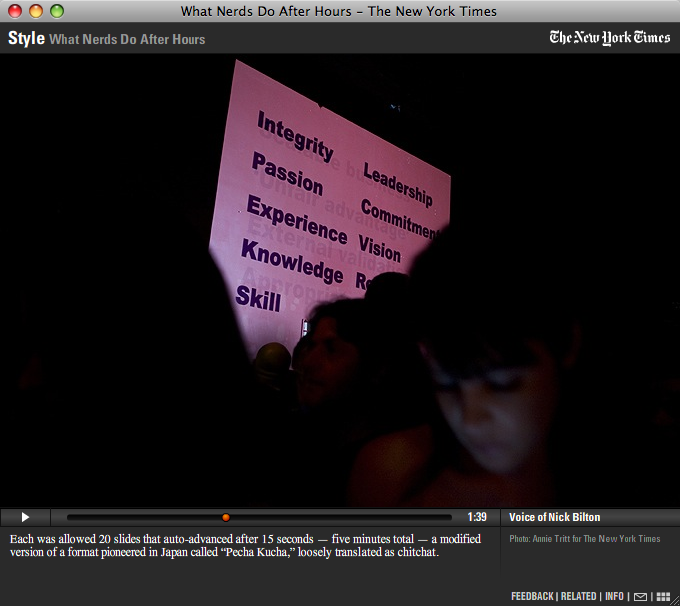

Although I haven't yet taken the time to blog about this one yet, it has been a staple of my business school lectures (and was captured by the New York Times during my Ignite presentation last month). In a nutshell, I have found that most investors look for the following ten 'must-haves' (pretty much in this order) in their search for the Perfect Entrepreneur: Integrity, Passion, Startup Experience, Domain Expertise, Functional Skills, Leadership, Commitment, Vision, Realism and 'Coachability'.

3) The Entrepreneur/Investor Disconnect on Returns

My point here was that even if you could get a typical entrepreneur and a typical investor to agree on the same target investment return for the investor (say, 25% IRR, as a reasonably high return for investing in a really risky startup), there is a gaping chasm between the two, because the entrepreneur looks at the question in light of his or her own venture, whereas the investor looks at it in light of his or her entire portfolio. The result is that the entrepreneur has heart attack when, having come to such an agreement, the investor says, "great, now that, of course, means that I need to get thirty times my money back from YOUR company! I've gone through the math in detail on my blog, but a crib note version is available over on Center Networks from a presentation I gave last Spring.

1) The Most Important Person on the Startup Team

In a blog post that I wrote on the subject after it came up in a conversation on the nextNY mailing list, I posit that it's not "the techie", nor "the UI person" nor even "the biz guy"...but rather The Entrepreneur... someone with a special set of skils and characteristics that may—or may not—be co-resident with the other functional skills mentioned above.

2) The Ten Crucial Attributes of an Entrepreneur

Although I haven't yet taken the time to blog about this one yet, it has been a staple of my business school lectures (and was captured by the New York Times during my Ignite presentation last month). In a nutshell, I have found that most investors look for the following ten 'must-haves' (pretty much in this order) in their search for the Perfect Entrepreneur: Integrity, Passion, Startup Experience, Domain Expertise, Functional Skills, Leadership, Commitment, Vision, Realism and 'Coachability'.

{kind=link}

3) The Entrepreneur/Investor Disconnect on Returns

My point here was that even if you could get a typical entrepreneur and a typical investor to agree on the same target investment return for the investor (say, 25% IRR, as a reasonably high return for investing in a really risky startup), there is a gaping chasm between the two, because the entrepreneur looks at the question in light of his or her own venture, whereas the investor looks at it in light of his or her entire portfolio. The result is that the entrepreneur has heart attack when, having come to such an agreement, the investor says, "great, now that, of course, means that I need to get thirty times my money back from YOUR company! I've gone through the math in detail on my blog, but a crib note version is available over on Center Networks from a presentation I gave last Spring.

Journalists and Business

Was talking with Jeff Jarvis, Anthony Moor, and another professional this evening at the Online News Association conference about journalists studying business issues. While Jarvis, who teaches an entrepreneurial journalism course, (rightly) said journalists don't need MBA-level business training, he and I agreed business acumen is needed. The question, though, came up of how to convince journalists they should learn anything about the business side. (I don't see the divider like I once did.) Here's one answer:

Only a fool doesn't care about the value of his work. And one of the best ways to understand the value being placed on what you do is to understand the ways business people think about it. That way, you have a much better chance of making sure you continue to have work to do, that it's sustained.

Openness Comes to Money

Having been around VCs and private equity (sometimes because my company helped construct strategy for a private equity events company), I'd sometimes thought that this often clubby, personally connected (and largely white and majority male) group of money purveyors was ripe to have their proprietary and costly databases chipped away at if not blown apart by someone who would make the data more open. Now "A VC" Fred Wilson points out that Angelsoft is showing industry data and that his firm would be glad to contribute to make it better.

He also notes that his Union Square Ventures doesn't subscribe to the expensive industry databases because they already have a good read of the market.

Silicon Alley Insider is doing something conceptually similar, analyzing SEC statements and industry trends, and making the information available for free, rather than keeping it paid and proprietary as Wall St. firms' research departments do.

Silicon Alley Insider is doing something conceptually similar, analyzing SEC statements and industry trends, and making the information available for free, rather than keeping it paid and proprietary as Wall St. firms' research departments do.

The Power of "Yes"

"If you go to sleep a Yankee fan, chances are you wake up one." That was the way keynote speaker Leo Hindery today helped explain why the Yes network is more profitable than any regional sports network every constructed. Except for four nights this baseball season, Yes was the highest rated network in 8 million homes with a 3.5-4 rating night after night, he said. ("And we were playing some crap teams!")

Speaking at the Convergence 2.0 conference put on by The Deal, Hindery, managing partner at InterMedia Partners, talked about the power of enthusiast media, how hunters and fisherman pore over their magazines and all other media, how they defined "engagement" – a "dedicated, committed audience." That kind of audience, he said, is key when looking for media investments. Look for a dedicated audience – Yankee fans, Christians, Hispanics (noting that all Hispanics are not alike), outdoorsmen – some group that will avidly consume what you give them, if you give it to them in their sweet spot.

The other thing you need, he said, to really have a lasting investment over time is barriers to competition, lamenting the way cable TV had screwed up its customer service, for example niggling people over $20 worth of charges when their lifetime value was, perhaps, $2,000. "There was no reason for the satellite industry to get going except for our ineptitude in cable," he said.

Speaking at the Convergence 2.0 conference put on by The Deal, Hindery, managing partner at InterMedia Partners, talked about the power of enthusiast media, how hunters and fisherman pore over their magazines and all other media, how they defined "engagement" – a "dedicated, committed audience." That kind of audience, he said, is key when looking for media investments. Look for a dedicated audience – Yankee fans, Christians, Hispanics (noting that all Hispanics are not alike), outdoorsmen – some group that will avidly consume what you give them, if you give it to them in their sweet spot.

The other thing you need, he said, to really have a lasting investment over time is barriers to competition, lamenting the way cable TV had screwed up its customer service, for example niggling people over $20 worth of charges when their lifetime value was, perhaps, $2,000. "There was no reason for the satellite industry to get going except for our ineptitude in cable," he said.

Thoughts on an 'Octopus' Strategy for Newspapers

It's not news that "if you take out classified ad profits from newspapers, you take out the profit." Those were the words today of Michael Price, Senior Managing Director at private equity firm Evercore Partners, at the Convergence 2.0 conference in New York put on by deal-watching publication The Deal. But he didn't leave it there, and instead talked about what to do – at least for one anomalous newspaper with an audience most publishers would kill for.

Price went on to talk about what his firm would do if they'd bought the Wall Street Journal: "go deep on the Internet" for their passionate, C-level (meaning top executive) audience, giving everything they could want about any of various subjects they're interested in, be it credit markets, insurance, or whatever. He called it an "octopus" strategy. Unfortunately, Price said, newspapers haven't figured out how to "monetize" their good content. Leo Hindery of InterMedia Partners in a keynote Q&A said the New York Times should follow a similar strategy, out-Googling Google by, for example, giving someone searching for news on Alan Greenspan everything they could possibly imagine. Instead, he said, they're putting their newspaper content online, but in a much more fragile ad banner market.

Jeffrey Sine of UBS Securities said that while the Journal is held up as a huge success for subscriptions on the Internet, it "really is not that successful in the larger sense," which I take to mean $70 million (1 million people paying $70 per year) isn't tons of money in this realm. He added on Price's remarks saying the Journal needed to "upsell" folks on their "tiered" interest levels by selling them more on the value chain. Sine said his firm had sold Marketwatch to Dow Jones a few years back (for nearly $500 million, if you remember), which I guess gave him Street cred.

Later, Price said that that Dow Jones and Reuters have been "crushed" by Bloomberg. Another panelist – Dennis Miller of Spark Capital -- pointed out how CNN ended its 27-year relationship with Reuters, probably because Reuters was directly competing by running its material directly, with its own ads. Hindery said the folks at Bloomberg "are not unapprehensive" about the lack of a print partner.

Price went on to talk about what his firm would do if they'd bought the Wall Street Journal: "go deep on the Internet" for their passionate, C-level (meaning top executive) audience, giving everything they could want about any of various subjects they're interested in, be it credit markets, insurance, or whatever. He called it an "octopus" strategy. Unfortunately, Price said, newspapers haven't figured out how to "monetize" their good content. Leo Hindery of InterMedia Partners in a keynote Q&A said the New York Times should follow a similar strategy, out-Googling Google by, for example, giving someone searching for news on Alan Greenspan everything they could possibly imagine. Instead, he said, they're putting their newspaper content online, but in a much more fragile ad banner market.

Jeffrey Sine of UBS Securities said that while the Journal is held up as a huge success for subscriptions on the Internet, it "really is not that successful in the larger sense," which I take to mean $70 million (1 million people paying $70 per year) isn't tons of money in this realm. He added on Price's remarks saying the Journal needed to "upsell" folks on their "tiered" interest levels by selling them more on the value chain. Sine said his firm had sold Marketwatch to Dow Jones a few years back (for nearly $500 million, if you remember), which I guess gave him Street cred.

Later, Price said that that Dow Jones and Reuters have been "crushed" by Bloomberg. Another panelist – Dennis Miller of Spark Capital -- pointed out how CNN ended its 27-year relationship with Reuters, probably because Reuters was directly competing by running its material directly, with its own ads. Hindery said the folks at Bloomberg "are not unapprehensive" about the lack of a print partner.

Even for Money Guys, It's About the Operations

It can be easy to the think of the money guys as doing deals and paying attention to the income, but not the operations. At today's Convergence 2.0 conference, run by The Deal, Josh Steiner, managing principal of private equity firm Quadrangle, disabused the audience of that notion when talking about how they handled Maxim after buying Dennis Publishing. Quadrangle brought in Kent Brownridge, a former top honcho at Wenner media who helped run Rolling Stone, and Dan Rosensweig, who had been COO of Yahoo! for the digital side to help bring "new skills and perspective" for an audience that moves freely between print and online, Steiner said. Brownridge helped renegotiate printing contracts. Anyone in the biz knows that those contracts can mean the difference between operating profit or loss.

"With all due respect to former management, they had a great run of it, and they were no longer doing the basic things with respect to blocking and tackling perspective," Steiner said, referring – for those of you who may not know American football – to the basics of playing the game.

"With all due respect to former management, they had a great run of it, and they were no longer doing the basic things with respect to blocking and tackling perspective," Steiner said, referring – for those of you who may not know American football – to the basics of playing the game.

Subscribe to:

Posts (Atom)